If you’ve been on social media lately, you’ve probably seen posts claiming that a new federal rule just changed how roofs are insured.

Let’s clear that up right away:

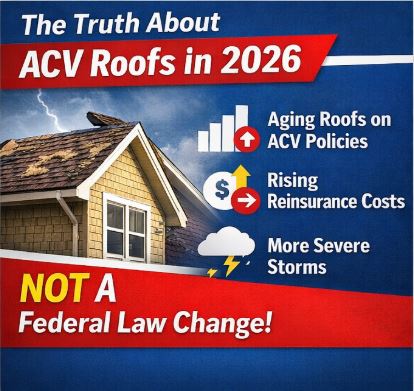

There has NOT been a single federal law change forcing insurance companies to switch to ACV (Actual Cash Value).

But here’s where things get real…

What’s Actually Happening (And Why It Matters)

Insurance companies are changing how they cover roofs—but not because of one law.

Across the country (including here on the Mississippi Gulf Coast), carriers are:

- Moving older roofs (typically 8–15+ years) to ACV coverage

- Limiting or removing full replacement cost policies

- Tightening underwriting guidelines

This is happening quietly—and it’s already affecting homeowners.

Why Insurance Companies Are Doing This

This shift is being driven by real financial pressure inside the insurance industry:

1. Loss Ratios Are Climbing

Storm claims are costing insurers more than they collect in premiums.

2. Reinsurance Costs Are Exploding

Insurance companies buy their own insurance (reinsurance), and those costs have skyrocketed.

3. Increased Storm Frequency

More hail, wind, and hurricane events = more payouts.

The result?

Insurance carriers are reducing their risk—and your roof is one of the first places they do it.

What ACV Actually Means for Homeowners

Let’s break this down in simple terms:

- Replacement Cost (RCV): Pays for a new roof at today’s price

- Actual Cash Value (ACV): Pays what your roof is worth after depreciation

Real Example:

- Roof replacement cost: $18,000

- 12-year-old roof

- Insurance payout (ACV): ~$6,000–$8,000

That leaves the homeowner responsible for the difference.

Why This Matters on the Mississippi Gulf Coast

Here in coastal areas like Biloxi, Gulfport, and Ocean Springs:

- Roofs age faster due to heat, humidity, and storms

- Wind exposure increases damage risk

- Insurance carriers are more aggressive with policy restrictions

Meaning homeowners here are more likely to be placed on ACV policies sooner

How to Protect Yourself as a Homeowner

If you own a home, here’s what you should do right now:

1. Check Your Policy

Look specifically for:

- “Actual Cash Value” vs “Replacement Cost”

- Roof age limitations

- Wind/hail endorsements

2. Know Your Roof Age

Once your roof crosses that 8–15 year range, your risk of ACV increases significantly.

3. Consider Upgrades That Matter

Stronger systems (like fortified roofing methods) can:

- Improve insurability

- Potentially reduce premiums

- Extend coverage eligibility

What We’re Seeing Every Day

At Ensured Roofing, we’re already seeing:

- Homeowners shocked by low claim payouts

- Policies switching to ACV at renewal

- Partial approvals turning into out-of-pocket expenses

This isn’t a future problem. It’s happening right now.

Final Thoughts: Don’t Fall for the Headlines

There was no sudden federal rule change.

But there is a major shift happening in the insurance industry—and it directly affects your home, your wallet, and your ability to recover after a storm.

The homeowners who stay informed and proactive will be the ones who avoid getting caught off guard.

Call to Action

If you’re unsure what your policy covers or how your roof would be handled in a claim:

We’ll review it with you and give you straight answers.

📍 Serving the Mississippi Gulf Coast

📞 228-797-7667

🌐 ensuredroof.com